It is essential for every accounting student to understand the definition, significance, and benefits of accounting.

In business, accounting serves as a communication tool by capturing financial transactions over a defined period and expressing them in monetary terms. The process involves recording, classifying, summarizing, and reporting the financial transactions of an organization.

The recording process involves creating and maintaining journals and subsidiary books,

Classification involves organizing transactions into relevant ledgers.

In the summarization process, trial balances and financial statements like balance sheets and profit and loss accounts are prepared to provide an overview of the organization's financial position and performance.

The accounting process for businesses follows the double-entry system, which means that every transaction has two sides: debit and credit. In other words, for every debit, there must be a corresponding credit, and vice versa.

This system ensures that each transaction is accurately recorded and helps maintain the balance of accounts. Additionally, if there is an increase in one account, there must be a corresponding decrease in another account, in order to keep the accounting equation balanced.

The process involves recording financial transactions using journal entries, ledgers, and trial balances. Financial statements such as balance sheets and profit and loss accounts are then prepared to present an accurate overview of the organization's financial performance. Additionally, accounting helps identify a business's financial position by analyzing its balance sheet.

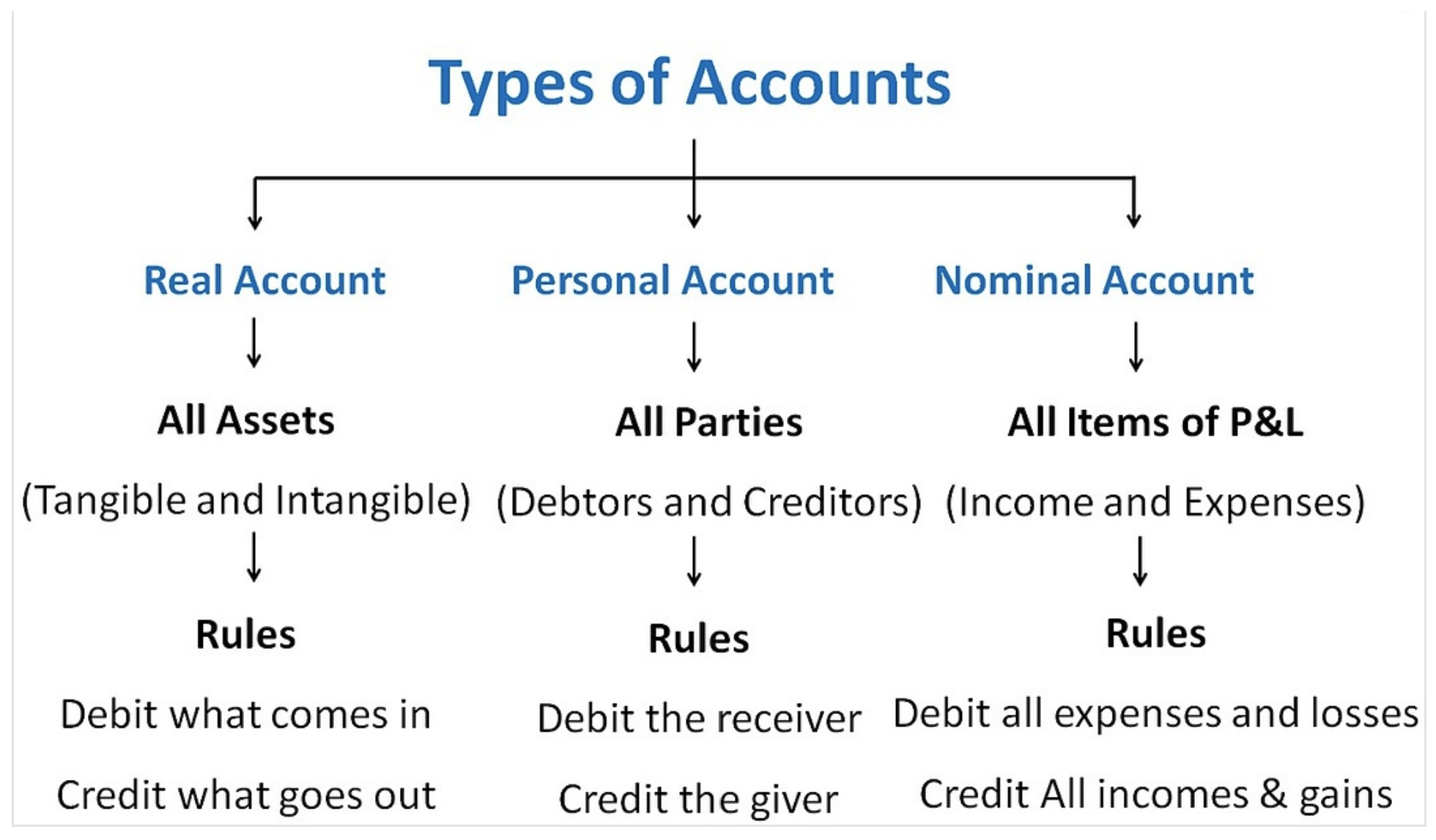

Types of Accounts

In accounting, there are three main types of accounts:

- Personal Accounts: These accounts represent individuals, organizations or groups with whom a business has a financial relationship. Examples include accounts receivable (amounts owed to the business by customers), accounts payable (amounts owed by the business to suppliers), and owner's equity (the amount the owner has invested in the business).

- Real Accounts: These accounts represent tangible assets such as property, equipment, inventory, and cash. These accounts are also known as permanent accounts because they are not closed at the end of an accounting period.

- Nominal Accounts: These accounts represent expenses, revenues, gains, and losses. Examples include sales, rent, wages, and interest expenses. The balances in nominal accounts are usually closed at the end of each accounting period and transferred to the retained earnings account.

Understanding the different types of accounts is important for accurate financial reporting and analysis. By properly classifying transactions into the appropriate accounts, businesses can monitor their financial health and make informed decisions.

The debit and credit accounts rules are based on three types of rules, which are also called as types of accounts in accounting. The different account types are

- Personal Accounts

- Real Accounts

- Nominal Accounts

Personal Accounts

Personal accounts itself refer to a name of person and it represents an Individual or Company or any Organization.

E.g of Personal Accounts: Datamug's Account, Customers account, etc.

Rules of Personal Accounts

If a person receive something in cash or goods, transaction will be debited and if a person gives something in cash or goods, than transaction will be credited.

- Debit the receiver

- Credit the giver

Example 1: Datamug paid £10,000 to Google cloud for hosting.

| Date | Particulars | Amount | Amount | Rule Applied |

| 20-Jun-22 | Google Cloud | 10000 | Debit the Receiver | |

| 20-Jun-22 | To Bank Account A/c | 10000 | Credit the Giver |

Real Accounts

Real Accounts refer to an assets owned or possessed by business. This real accounts reveals the valuation and movement of assets that occurred between firm and other parties. Assets can be real assets or intangible assets.

- E.g. of Real assets : – Buildings, Furniture, Machines, etc.

- E.g of Intangible assets: – Goodwill, trademarks, etc

Rules of Real Accounts

The assets that are coming in to business, transaction will be debited. If the assets are going out of business, than the transaction will be credited.

- Debit what comes in

- Credit what goes out

Example: Purchased computers on 10th June 2022 for £2000 in Cash

| Date | Particulars | Amount | Amount | Rule Applied |

| 10-Jun-22 | Computer A/c | 2000 | Debit what comes in | |

| 10-Jun-22 | To Cash Account A/c | 2000 | Credit what goes out |

Nominal Accounts

Nominal accounts are temporary accounts that related to incomes, expenses. revenues and losses of business. Nominal accounts are mainly deal with the amount of income earned and expenses/costs incurred. It records all expenses and incomes which are not carried forward to future.

E.g. of Nominal Accounts: – Sales, cost of goods, rent, interest, etc

Rules of Nominal Accounts

The expenses and losses of business transactions are debited, and the gains and profits of business are credited.

- Debit all expenses and losses

- Credit all gains and profits.

Example: Purchase of goods for £3,000 in Cash.

| Date | Particulars | Amount | Amount | Rule Applied |

| 10-Jun-22 | Goods A/c | 3000 | Debit all expenses | |

| 10-Jun-22 | To Cash Account A/c | 3000 | Real A/c – what goes out |